Yesterday, the Congressional Budget Office put out an SOS

In the next few decades, the federal debt is expected to rise to the highest level since World War II.

And that this could increase the risk of a fiscal crisis.

One key reason for the uptick: the gov spending more on things like Medicare and Social Security.

Here an article on this theme from Politico:

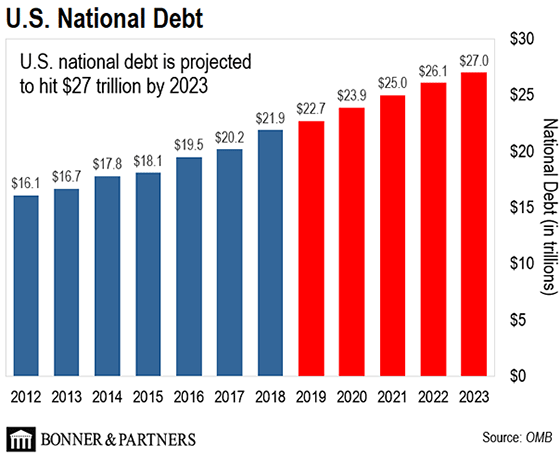

Federal debt held by the public is already sky high and it’s expected to soar during the next 30 years if current laws remain unchanged — dramatically escalating the risk of a “fiscal crisis,“ the CBO said in a new report Tuesday.

Debt held by the public is projected to rise from 78 percent of gross domestic product this year to 144 percent by 2049, according to long-term budget projections released by CBO.

The agency noted that such debt over the last 50 years has averaged 42 percent of GDP, exceeding 70 percent during only one other period in U.S. history — after the “surge in federal spending that occurred during World War II.”

CBO’s projections not only assume that current laws stay in place, but that benefits through federal safety net programs like Social Security and Medicare are paid in full even if the programs are nearing or have reached insolvency.

If the U.S. stays on this path, economic output would suffer over time, the agency said. That path would also “increase the risk of a fiscal crisis — that is, a situation in which the interest rate on federal debt rises abruptly because investors have lost confidence in the U.S. government’s fiscal position.”

Higher interest costs, driven by a major increase in federal borrowing and higher interest rates over the long term, are key drivers of the country’s long-term budget woes, said CBO Director Phillip Swagel. Other significant drivers are an aging population, rising health care costs and greater federal spending on Social Security and Medicare.

The agency’s projections could vary greatly depending on how Congress acts on fiscal policy. For example, if Congress prevented $126 billion in sequestration cuts next year and an increase in individual income taxes in 2026, debt held by the public would be even higher, reaching 219 percent of GDP in 30 years.

House and Senate leaders haven’t made headway on a deal to avoid billions in mandatory spending cuts next fiscal year, increasing the likelihood of a scramble to extend current funding levels when the federal government runs out of money at the Sept. 30 end of the fiscal year.

[Politico]

{kind=link}